Discover the Intersection of

Collections and AI

Built to perform across the customer journey.

How Skit.ai integrated AI debt collection with IDMS to automate conversations and vehicle hardware control, halving delinquency and scaling the book 30% without adding a single agent.

Headquartered in Oklahoma, the Lender is a vertically integrated automotive group operating two connected verticals, i.e., a network of in-house dealerships selling new and pre-owned vehicles, and a captive auto-finance arm that underwrites the loans for buyers who finance their purchase in-house. The business model is built on interest yield from financed vehicles which makes early-bucket collections health a direct driver of revenue, not a back-office function.

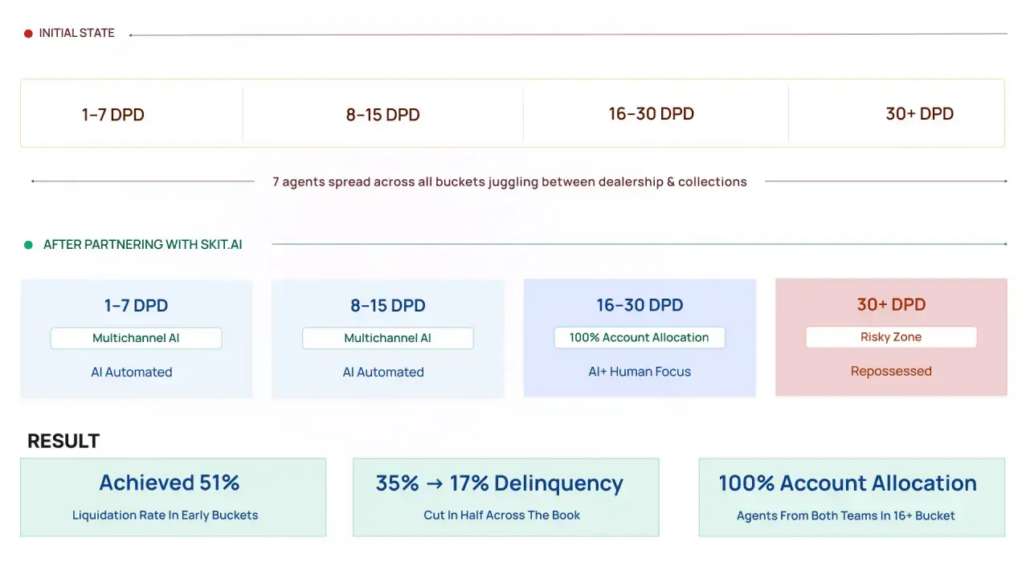

The Lender operates a weekly-cadence delinquency framework with four DPD buckets. The 30+ DPD bucket is the repossession threshold, once an account rolls past 30 days, the vehicle is recovered, and the original lending thesis turns into a hard loss against the book.

The Lender partnered with Skit.ai with a single overriding goal, i.e, scale early-bucket collections capacity without growing the in-house team, and contain rollovers before they reach the 30+ DPD repossession zone.

The problem was operational, not behavioral. Borrowers were not refusing to pay, rather the system around them was creating delinquency and friction faster than a stretched team could resolve it. Building a separate contact center wasn’t an option. Adding agents linearly wasn’t either.

| Behaviour | Insight | Actions Taken |

|---|---|---|

| Payday timing | Borrowers paid on their actual payday, not their EMI due-date. Friday payers were repeatedly going 1-DPD on Monday-due EMIs through no intent of missing. | Bot detected pay patterns on-call and triggered EMI date restructuring in IDMS turning artificial delinquency into on-time payment. |

| Reason mix for missed payments | Borrowers consistently cited verifiable hardships, i.e, job switch, pay-period shifts, medical events, severe weather, broken vehicles, rather than refusal to pay. | Bot was trained to recognise these reasons, capture documentation, and route them: due-date change to the in-house team, broken vehicles to the nearest dealership/workshop. |

| Bucket-to-bucket rollover | Once an account rolled past 15 DPD, in-house contact-to-resolution rates dropped sharply, making 1–15 the most cost-efficient intervention window in the book. | Skit.ai bot took primary coverage of 1–15 DPD with high-frequency attempts. Three in-house agents were redeployed exclusively to 16+ DPD. |

| Vehicle unlock latency | Manual unlock tickets meant Sunday-night payments left cars disabled until Monday morning. A customer-experience hit and a recovery delay. | Vehicle enable/disable wired directly to IDMS via API. Payment validates in real time and the car unlocks the same evening. |

| 30+ DPD = Repossession | Every account that rolled past 30 DPD became a repossession candidate; charge-off at 60 DPD compounds the loss. Both are direct hits to the interest-yield model | The full collections strategy was re-anchored around rollover containment keeping accounts below 16 DPD to protect downstream repossession and charge-off exposure. |

| Agent-to-agent quality variance | Across the in-house team of 7 agents were stretched between dealership and collections, call quality varied significantly. Compliance, negotiation, and handoff discipline drifted account to account. | Single specialised bot policy across every interaction was applied. Same compliance level, same negotiation discipline, same scripted handoff. 88%+ of calls now run end-to-end without human involvement. |

Skit.ai’s automated collections software was deployed across the rollover edges of the weekly EMI book. Phased bucket-by-bucket expansion across voice, SMS, and email, AI-led coverage of the early-bucket containment window, and the entire vehicle disable/enable hardware loop wired into the same IDMS API surface as the conversation. The deployment exercised the full range of Skit.ai’s automated debt collection software integration capabilities, handling both real-time payment processing and vehicle locking through a unified debt collection management software interface.

88%+

Bot Managed Calls

Human Handled Only On Complex 15+ DPD Cases

51%

Liquidation Rate

Achieved On Early Buckets

30%

Of Portfolio Expansion

Over Engagement

35% → 17%

Delinquency Cut

In Half Across the Book

The client’s challenge was purely operational. Weekly EMIs meant missed Sunday payments hit 1-DPD by Monday, leaving a small team of seven overstretched between dealerships and collections. Furthermore, manual hardware triggers meant Sunday payers remained locked out of their vehicles until Monday morning.

Skit.ai integrated voice, SMS, and email bots into the lender’s IDMS via a single API to automate the cycle. The AI now aligns EMI dates with borrower paydays and triggers automatic vehicle unlocking immediately upon payment. For accounts past 15 DPD, the bot offers settlements or routes hardships to dealerships, allowing agents to focus 100% on high-priority 16+ DPD cases. Today, 88% of calls are handled end-to-end with superior consistency and compliance.

Hence to wrap it up, “Cars and collection conversations both needed automation. Neither could grow manually.”

Built to perform across the customer journey.