Discover the Intersection of

Collections and AI

Built to perform across the customer journey.

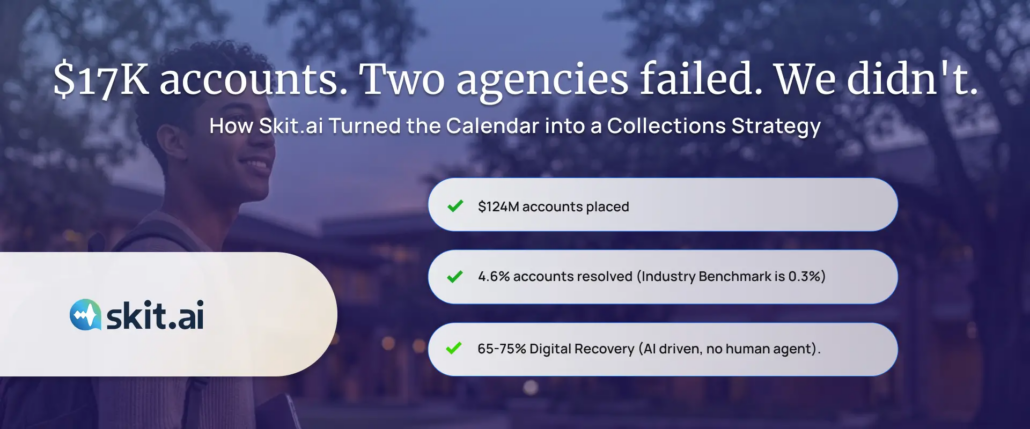

How Skit.ai used AI for Collections to turn New Year resolutions, tax refunds, and Christmas into a recovery strategy for $124M in education loans.

A U.S. based private lender specialising in high-ticket education loans for graduates of professional programmes and specialised schools, addressing a critical gap as federal loans often fall short of covering the full cost of advanced degrees in law, medicine, business, and engineering. It bridges this gap through high-value lending tailored to borrowers’ long-term earning potential rather than their current financial position. To scale and optimize recovery for this unique borrower profile, the lender partnered with Skit.ai to deploy a unified, Al-powered omnichannel platform built for scale and compliance.

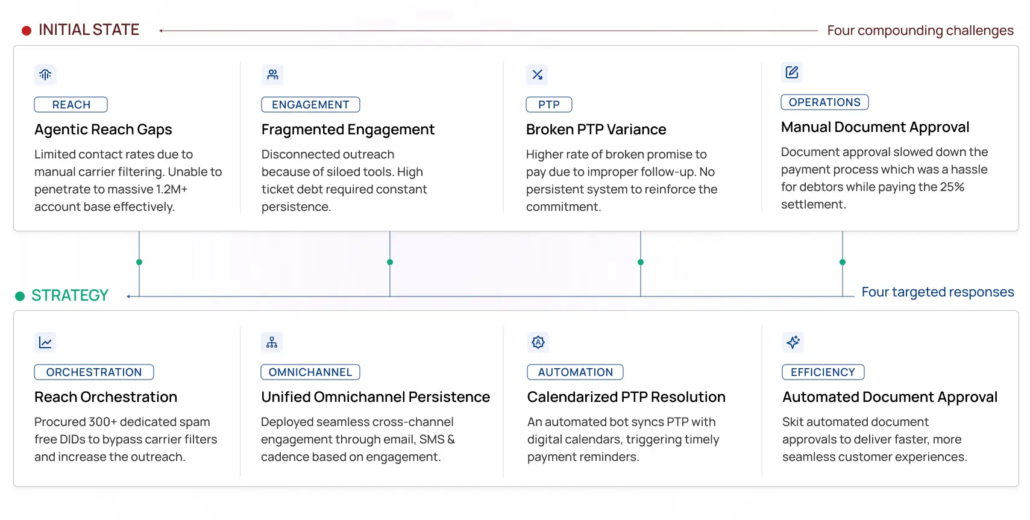

Agentic reach gaps restricted scalable outreach across a 1.2M+ account base, leaving a significant number of accounts unengaged and aging without intervention. At the same time, fragmented engagement across siloed tools led to inconsistent communication, lack of a unified customer view, and ineffective follow-ups, limiting overall outreach impact. Broken promise-to-pay (PTP) commitments, without automated tracking or enforcement, further weakened recovery outcomes as commitments were not consistently honored. Additionally, manual document approval processes introduced last-mile friction, delaying conversions even for borrowers ready to pay. Compounding these challenges, behavioural barriers, particularly misconceptions around minimum payment expectations discouraged borrowers from initiating engagement, ultimately suppressing recovery performance across the portfolio.

The market challenge: According to the Federal Reserve’s 2024 Economic Well-Being report, median outstanding education debt among U.S. borrowers sits between $20k–$25k. Roughly 6 million Americans have fallen behind on student loan payments, a return to pre-pandemic delinquency levels. This lender’s borrowers have good intentions but face a compressed post-graduation window: income takes months to stabilise, job placements take time, and loan repayments arrive before paychecks do.

Before designing a single campaign, Skit.ai mapped the borrower segment end to end — how they earn, communicate, and engage with debt. Not a desk exercise. A deep dive that became the foundation for every design choice.

| Dimension | Insight |

|---|---|

| Channel preference | Email and SMS engagement in collections rose 9% year-on-year (TransUnion). 80% of consumers now prefer a fully digital debt-management experience — 25% engaging after 9 pm and before 8 am (TrueAccord). |

| Borrower profile | Recent graduates, averaging $17,000 in debt. Tech-savvy, income-constrained in early post-graduation months, willing to pay but easily deterred by perceived payment barriers. |

| Top engagement windows | New Year, U.S. tax-refund season, and Christmas — moments of financial motivation and psychological receptivity |

| What We Learned | What We Changed |

|---|---|

| Consumers prefer digital channels | Shifted primary outreach to SMS and email; reduced reliance on voice calls |

| Cash flow tied to seasonal events | Timed campaigns around New Year, tax-refund season, and Christmas |

| Minimum-payment confusion | Surfaced flexible, lower-entry payment options early in every outreach flow |

| Broken PTP loops | Automated reminders tied to each borrower’s own stated promise-to-pay date |

| Last-mile drop-offs at settlement | Automated document approval and bank-statement verification end-to-end |

The channel shift was non-negotiable. The borrower’s base — recent graduates, tech-savvy and income-constrained, reflected exactly the digital-first pattern the data confirmed. Southwood Financial partnered with Skit.ai to deploy a unified debt collection management software platform built for scale, compliance, and this specific borrower profile.

Borrower profiles were built around the typical recent graduate: ~$17k in debt, digitally comfortable, financially constrained in the early post-graduation window, and genuinely willing to pay. Flexible, lower-entry payment options were surfaced prominently and early in every outreach flow.

Over 300 dedicated, spam-free DIDs were procured to bypass carrier filters and penetrate the 1.2M+ account base that manual outreach couldn’t reach. A single unified platform ran cross-channel engagement — email, SMS, and cadence-based follow-ups — with a seasonal content strategy layered on top:

Settlement negotiations opened at a 20% discount versus the 25% borrowers initially requested — recovering better yield while still meeting borrowers where they were financially. Document approval (expense and bank-statement verification) was fully automated end-to-end, eliminating last-mile drop-offs. Every interaction carried full compliance: audit trails, consent management, and PTP records maintained automatically with zero manual oversight.

$124M

Accounts Placed

Total portfolio under management

4.6%

Accounts Resolved

Industry Benchmark : 0.3%

65-70%

Digital Recovery

AI-driven, no human agent

20%

Negotiated Settlement

vs. 25% requested — protecting yield

| Approach | What Changed | Outcome |

|---|---|---|

| Seasonal Content Strategy | Email templates built around New Year, tax-refund season, and Christmas — each timed to borrower motivation and financial receptivity. | Stronger open rates and payment conversion across all three seasonal windows. |

| Carrier Filter Bypass | 300+ dedicated spam-free DIDs procured to penetrate a 1.2M+ account base that manual outreach couldn’t reach. | Higher contact rates; more accounts reached and resolved. |

| Payment Flexibility Upfront | Lower-entry payment options surfaced early in every outreach flow, removing the minimum-payment misconception. | Borrowers who assumed they couldn’t afford to start found out they could. |

| Calendarised PTPs | Automated reminders tied to each borrower’s own stated promise-to-pay date, linked to their email ID. | Fewer broken commitments; improved payment follow-through across the book. |

| Automated Document Approval | Expense and bank-statement verification fully automated end-to-end. | No drop-offs at the final settlement stage; faster closures. |

| Negotiation Tactic | Settlement opened at 20% discount vs. the 25% requested by borrowers. | Better recovery yield per settled account without pushing borrowers away. |

This lender had a borrower base with genuine intent to pay and an outreach model that kept getting in the way. Siloed tools, broken PTP loops, and last-mile friction were turning resolvable accounts into legal cases.

Skit.ai modernized the lender’s debt collection management approach and went further. Seasonal content campaigns timed around New Year resolutions, tax-refund season, and Christmas brought a level of empathy and timing intelligence rarely seen in collections outreach. Borrowers weren’t chased. They were met at the right moment, with the right message, through the right channel.

As the Urban Institute research states, falling behind on loan payments carries long-lasting consequences: credit-score damage, loss of future credit eligibility, and the compounding stress of escalating collections. This is where modern AI debt collection strategies create measurable impact by delivering the right outreach at the right time, through the right channel. That’s exactly what Skit.ai delivered.

Built to perform across the customer journey.

From $60M in Aged Debt to 70% Email Open Rates: How Skit.ai Used AI for Debt...

From $60M in Aged Debt to 70% Email Open Rates: How Skit.ai Used AI for Debt...