Why Are We Still Collecting Like It’s 2010?

Billions in recoverable debt go uncollected every year—not because borrowers disappeared, and not because they flat-out refuse to pay. It’s because most collections teams are still using blunt-force tactics: same scripts, same cadences, same assumptions.

Treating every borrower the same is the fastest way to lose them.

AI-powered segmentation flips that on its head. It replaces guesswork with real signals—intent, timing, behavior—and delivers the right message to the right borrower, exactly when it matters.

If you’re still sorting accounts by balance size or days past due, you’re not just falling behind. You’re leaving recovery on the table.

How Smart Segmentation Rewires Recovery

At Skit.ai, we didn’t just theorize about borrower behavior—we studied it at scale. Analyzing over 14 million accounts across creditors, banks, and fintechs lenders, we uncovered a game-changing insight:

Borrowers don’t behave according to static labels like “30 days past due” or “FICO score 620.”

They behave according to something far more powerful—and often invisible: intent.

- Some customers want to pay but can’t yet.

- Some can pay but won’t—unless nudged at the right pressure point.

- Some are right on the cusp—waiting for a perfectly timed outreach to act.

This realization challenged and ultimately reshaped the old model of collections strategy.

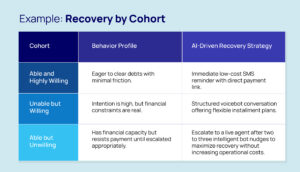

Instead of segmenting by superficial factors (balance size, loan age, credit score), Skit.ai’s Collection Intelligence Platform re-segments accounts based on a dynamic behavioral axis:

- Ability to Pay (Can they pay?)

- Willingness to Pay (Will they pay if contacted correctly?)

This produces 12 precision cohorts across 19 debt types, each with distinct psychological and financial profiles. Each cohort demands a custom recovery approach, not a one-size-fits-all call script.

How Our AI Predicts the Winning Moves

Unlike manual teams that rely on outdated heuristics, Skit.ai’s system learns from real-world interaction signals, such as:

- Payment promises vs payment fulfillment

- Call and SMS response patterns

- Engagement fatigue points

- Sentiment cues from conversations

Based on these signals, our platform dynamically recommends for each cohort:

- Best timing for outreach: Not just broad time windows, but personalized based on when an individual is statistically more likely to respond positively.

Most effective channel: Voice, SMS, email, or a smart sequence that adapts if initial channels do not yield engagement. - Tone and messaging: Choosing between a soft reminder, an urgent escalation, or a personalized negotiation offer depending on the behavioral data.

Recovery stops being a reactive guessing game.

It becomes an engineered sequence of micro-optimizations, tailored to the hidden psychology of each borrower.

The core insight is clear:

By speaking to each borrower differently—through the right channel, at the right time, with the right message—you unlock uplift and efficiencies that traditional blanket campaigns simply cannot achieve.

This is not a marginal improvement. It is a transformational uplift, delivering 50–70% better liquidation rates across real portfolios already living with Skit.ai’s platform.

The Only Results You Would Want to See

Traditional collections teams often chase liquidation rates with:

- Flat, script-based calls

- Generic cadence rules (e.g., “Call at Day 30, 60, 90”)

- Channel siloing (voice team vs email team)

In contrast, our AI platform takes a surgical approach. When Skit.ai’s segmentation engine is applied, recovery rates see an immediate jump:

That’s without adding a single new headcount to your team. The reason is simple: AI segmentation respects borrower behavior, allowing you to deploy human agents only when necessary, while bots handle scalable nudges and negotiations.

Timing is Everything (And AI Knows It Best)

One major blind spot in traditional collections is outreach timing.

Without real behavioral data, companies default to mass blasts: calling everyone in a single time window, regardless of likelihood to convert.

Skit.ai’s AI platform analyzes past engagement patterns to optimize not just who you contact, but when.

Example:

A cohort identified as “Willing but Anxious” showed 38% higher payment promise rates when contacted on Tuesday evenings versus Monday mornings. Manual teams would never catch that nuance—AI does, instantly.

This is why intelligent collections aren’t just “faster”—they’re exponentially smarter.

Charting a Smarter Path to Recovery

The collections landscape is evolving—and so are the tools leading it forward.

Creditors leveraging behavioral segmentation and AI-driven strategies aren’t just recovering more—they’re doing it faster, more efficiently, and with greater borrower empathy.

With over 53,000+ creditors already seeing 50–70% uplift in recovery rates, the momentum is clear: Precision is outperforming tradition.

As you plan your Q3 and beyond, consider what’s possible when segmentation aligns with strategy—when every outreach is timely, targeted, and tailored. Better liquidation is no longer a stretch goal. It’s a smart, data-backed next step.

Ready to Take the Long View with AI in Collections? Let’s talk.